Monday, January 31

Sunday, January 30

The Buck Stops Here: Housing Price Trends and the Economic Outlook

Is the time finally right to get back into the residential real estate game? And what are the broader implications of trends in housing on the overall economy and financial markets? Let's take a look at the arguments and data.

The Case for Investing in Housing

Mortgage interest rates have come up some recently but are still near historic lows and appear attractive.

We're also entering the comparatively slow home buying season and prices, after a post-bubble popping uptick, have been retreating recently. There may be some sweet deals to be had over the next several months.

And perhaps most importantly are the following two considerations: a) the overall economy is showing increasing signs of life and b) the risk of deflation appears to be subsiding as commodity (e.g., oil) and food price inflation is taking off globally. Real estate has historically been considered one of the best ways to protect oneself against broad inflation.

Add it all up and it would appear that housing could in fact be a prudent investment right now. What would be reasons for holding off?

Continue reading the full article published on SeekingAlpha here.

The Case for Investing in Housing

Mortgage interest rates have come up some recently but are still near historic lows and appear attractive.

U.S. 30-Year Mortgage Interest Rates

|

| Note: chart data only runs through early 2010; if updated through 2011 the chart would show a recent increase in interest rates to around 5%. |

We're also entering the comparatively slow home buying season and prices, after a post-bubble popping uptick, have been retreating recently. There may be some sweet deals to be had over the next several months.

And perhaps most importantly are the following two considerations: a) the overall economy is showing increasing signs of life and b) the risk of deflation appears to be subsiding as commodity (e.g., oil) and food price inflation is taking off globally. Real estate has historically been considered one of the best ways to protect oneself against broad inflation.

Add it all up and it would appear that housing could in fact be a prudent investment right now. What would be reasons for holding off?

Continue reading the full article published on SeekingAlpha here.

Friday, January 28

Mind of a Hedge Fund Manager: Inside Hugh Hendry's Head

|

| The Eclectica Chief holding court |

During this week's Alternative Investment Conference in London, the iconoclastic speculator waxed philosophical about his own "self loathing" and the "voices inside his head", described indirect ways to play the Chinese property bubble, and explained how desperate he is to "see inside the envelope waiting in the future which contains my 10-15-20 year performance results".

Hendry's keynote was facilitated by author Steven Drobny, who explained that his goal for this interview was to "get inside the head of Hugh Hendry". Also of note, Drobny publicly revealed for the first time that Hendry was in fact the anonymous 'Plasticine Man' featured in his recent book Invisible Hands: Top Hedge Fund Traders on Bubbles, Crashes, and Real Money.

While Hendry declined Drobny's Freudian-esque invitation to recline on a couch brought up on stage specifically for him, he did play along with Drobny's word association game. When prompted with the names Ben Bernanke and Vladamir Putin, the same two words popped out of Hendry's mouth: "evil genius". What does that reveal about the way Hendry thinks? Perhaps not as much as the below conference highlight reel which was dubbed "Hugh Hendry's Greatest YouTube Hits".

Hendry's growing notoriety has managed to attract attention on the other side of the pond. In a NY Times profile last summer the Eclectica boss quipped “If there was a way to short Obama, I would”. At the conference he clarified that his remark was not directed at President Obama personally per se, just his policies.

For Hugh Hendry followers much of what he said at the conference may be familiar, but here are a few of the highlights:

- The euro is "mortally wounded but can limp on for awhile at the expense of ordinary people, making it expensive to speculate against".

- His best trades are the ones where he doesn't "fear the consequences of being wrong".

- He's not positive (bullish) on any country.

- In his own opinion, one of the keys to his success is that from an early age he was "taught to misbehave".

When it came to talking specific investments themes, Hugh outlined his bearish stance on China: "the only thing unique about China's economic strategy are the sheer numbers". Fundamental to his bearishness is the fact that so much capital in China has been directed for sovereign, rather than purely economic purposes.

He compared China to a "sun moving other planets", and that "it's best not to short the mainland but instead short the satellites" or "dark side of the moon" as he called it. As such Hendry has a significant "basket" of Japanese credit default swaps with a four year time horizon. He discussed the evolving Japanese steel industry and his expectation that Japanese steel exports will contract significantly in the years to come.

Like Jim Chanos, he is extremely bearish on Chinese commercial real estate and even provides a guided tour of empty Chinese high-rise buildings in the below video.

Whether or not Hendry's bets will pan out within his time frame is an open question. But what is without question is that the financial world is certainly a more interesting and entertaining place with the outspoken Hugh Hendry.

Thursday, January 27

Video: Exporting Propaganda - China's New Charm Offensive

|

| Spin, manufactured in China |

Yes, this bought and paid-for China is the same country which has banned its citizens from using Facebook, Twitter, YouTube, and most recently Skype. As noted by the NY Times, China's rulers are "obsessed with the threat posed by the Internet".

From the article:

Li Changchun, a member of China’s top ruling body, the Politburo Standing Committee, and the country’s senior propaganda official, was taken aback to discover that he could conduct Chinese-language searches on Google’s main international Web site. When Mr. Li typed his name into the search engine at google.com, he found “results critical of him."

A Chinese person with family connections to the elite (said) that Mr. Li himself directed an attack on Google’s servers in the United StatesIn the wake of the overthrow of Tunisia's government, other dictatorships (e.g., Mubarak's monarchy in Egypt) are now following China's lead.

I can only imagine how the Politburo Standing Committee's discussion over China's international image problem went down: "China is the world's greatest exporter, and propaganda works pretty well here, so why not package the two together?"

Twitter vs. Facebook: Which Was a Bigger Factor in Overthrowing Tunisia's Government?

|

| Viva la revolution! (a photoshopped Mark Zuckerberg) |

From the article:

There has been a lot of debate about whether Twitter helped unleash the massive changes that led Ben Ali to leave office on January 14, but Facebook appears to have played a more important role in spreading dissent.

"I think Facebook played a bigger role in this case," said Jillian York of the Berkman Center for the Internet and Society, who has been tracking the Tunisian situation closely. "There are a lot more Facebook users than Twitter users. Facebook allows for strong ties in a way that Twitter doesn't. You're not just conversing."The Atlantic article also addresses Facebook's response to attempted hacks, presumably by the notorious Ammar (Tunisia's secret police operation).

From Facebook's Chief Security Officer Joe Sullivan:

"We get requests all the time in a few different contexts where people would like to impersonate someone else. Police wanting to go undercover or human rights activists, say," Sullivan said. "And we, just based on our core mission and core product, don't want to allow that. That's just not what Facebook is. Facebook is a place where people connect with real people in their lives using their real identities."Anyone still wondering why in addition to Twitter and Facebook, China also blocks its citizens from using YouTube and Skype?

Tuesday, January 25

Review Roundup: Inside Job (The Movie)

If you have not already had the chance to see it I cannot recommend this film highly enough. It pulls off the not so easy feat of both clearly explaining the financial crisis in sufficient detail while managing to keep your attention throughout.

(Update: Inside Job is an Oscar nominee for Best Documentary. The below list will be updated regularly with additional reviews and please feel free to post links in the comments)

Here's a roundup of some of the film's reviews which I'll try and regularly update as more reviews come in:

Guardian

Felix Salmon

Naked Capitalism / Yves Smith

New Yorker

The New Republic

LA Times

Rotten Tomatoes

And some additional reviews from Yahoo Movies:

| |||||

Source | Brief Review | Grade* | |||

| Boston Globe Wesley Morris | "The movie succeeds at upsetting you not by losing its cool, the way so many similar films do, but by slow-cooking its argument." | A | |||

| Chicago Sun-Times Roger Ebert | "...an angry, well-argued documentary about how the American financial industry set out deliberately to defraud the ordinary American investor." | A | |||

| Filmcritic.com Chris Cabin | "Like No End in Sight, the key to Inside Job's power is how clearly Ferguson maps out each step towards disaster..." | B | |||

| New York Times A. O. Scott | "...meticulous and infuriating..." | A- | |||

Monday, January 24

U.S.-China Currency War: Should America Fight Back by Defaulting?

|

| A little less handshaking, a little more action? |

'Bleeding-hearts' types will no doubt want to focus on human rights issues, such as China's not so secret effort to wipeout Tibetan civilization and the ongoing imprisonment of China's recent Nobel Peace Prize winner, Liu Xiaobo.

As the NY Times opinion page put it, "how can one Nobel Peace Prize laureate be silent when meeting the man who imprisons the next?"

And those concerned with the military balance of power can point to concerns about Chinese espionage, secret development of sophisticated weaponry like a Chinese stealth fighter, and China's navy contesting free navigation in the South Sea.

The Renminbi Runaround

There is also the matter of U.S.-China economic relations. As far as the U.S. is concerned, the big one is the exchange rate of China's currency, the renminbi (yuan). It is widely agreed that China's currency is undervalued by as much as 20-40%, providing China with an unfair trade advantage. Much has been written about this issue previously here.

Former Secretary of State and and National Security Advisor, Henry Kissinger, appeared on Charlie Rose this week to discuss relations with China. Not surprisingly, Kissinger argued for a diplomatic solution to the renminbi. While acknowledging that he is not economist, Kissinger believes there should be some way to bring the Chinese around on revaluing the renminbi by offering something in return. My question is hasn't the U.S. already tried that ad nauseam?

Throughout modern history the world's trade and currency order has always followed a set of explicit and implicit 'rules of the game', so to speak. Over the last two decades China has benefitted significantly from first having access to the world's markets and later gaining entrance into the World Trade Organization. While WTO rules do not cover exchange rate manipulation, one of the hallmarks of our current semi-free trade system is floating exchange rates. China exercises heavy control over its exchange rates in a manner completely unlike other major trading powers, such as the U.S.

The key question, put simply, can be expressed as follows: why is there one set of currency rules for China, and another set for everyone else?

Continue reading the full article published on SeekingAlpha here.

Sunday, January 23

Economic Newspeak: Has Yale's Robert Shiller Seen the Light?

"To me...part of the process of pursuing the inexact aspects of economics is speaking honestly to the broader public, looking them in the eye...and then searching one’s soul to decide whether one’s favored theory is really close to the truth."

-Robert Shiller, Project Syndicate Op-ed January 20, 2011

|

| Yale Professor Robert Shiller |

Yves Smith over at Naked Capitalism also took exception when Shiller's November op-ed came out, characterizing the Yale Professor's argument as a justification for Orwellian newspeak.

Shiller previously argued that terms like 'bailout' should be recast as ‘orderly resolutions’ so as to make sure the voting public 'gets it'.

From Shiller's November piece:

When life is smooth, people tend to remain complacent, reflecting confidence in the economy. In times of crisis, such confidence is also vital, even if government can’t absolutely guarantee that it’s justified.

...well-thought-out framing packages can work. They can help sell crucial intervention packages to people who don’t fully understand the financial system’s complexities.As I noted in my response to Shiller:

In other words, Shiller is making the argument that it's not only ok, but advisable for the government to be less than frank with voters. During a financial crisis, Shiller argues, this lack of candor is actually in the public's own good.

Putting aside the subject of the ethical responsibilities of public officials for a moment, the first question is would Shiller's recommendation even work?

To help answer that question we can turn to a recent example from early 2008, prior to the apex of the financial crisis. On March 28, 2008, Fed Chairman Ben Bernanke, testifying before Congress about the housing market, made the now infamous false assurance that the subprime real estate crisis was "contained".

There are two possibilities here: either a) the Fed Chairman honestly believed that the Fed's actions had magically put the breaks on the real estate meltdown; or b) he was consciously using propaganda to reassure people, as Shiller advocates.

Regardless of which of these two possibilites is correct, what we do know is that his reassurances did absolutely nothing to prevent the financial crisis, which hit full force later that year in September. Perhaps Bernanke's comment postponed the crisis, but postponement may in fact have made it worse by allowing the problem to further fester under a blanket of false Fed confidence.

Here's to hoping Shiller's more recent reflections indicate an about face in his thinking along with a commitment to speaking clearly and truthfully on economic matters, like taxpayer funded bailouts, with the general public.

Video: Niall Ferguson -- Will the Financial Crisis Lead to America's Decline?

Courtesy of FORA.tv, a July 2010 panel discussion with David Gergen, Mort Zuckerman and Niall Ferguson at the Aspen Institute broken out in subject chapters in the links below.

01. Introduction 05 min 08 sec

02. Financial Crisis Accelerated West to East Power Shift 07 min 50 sec

03. American Business Culture Is Healthy 06 min 44 sec

04. Threat of Rapid Decline 03 min 53 sec

05. Complexity Theory and National Strength 02 min 30 sec

06. Debt and Stimulus 03 min 22 sec

07. Innovation Only Helps by Creating Domestic Jobs 02 min 59 sec

08. Growing Education Gap 02 min 38 sec

09. A World Without a U.S. Superpower 04 min 55 sec

10. Q1: U.S. Headed Toward Capitalism or Socialism? 02 min 48 sec

11. Q2: What Happened to Budget Surplus 02 min 00 sec

12. Q3: Coping with China Graduating Thousands of Engineers 02 min 37 sec

13. Q4: How to Manage the Deficit 05 min 05 sec

14. Q5: Low Birth Rate in China 02 min 52 sec

15. Q6: Federal Reserve and Treasury Contribution to Crisis 03 min 26 sec

01. Introduction 05 min 08 sec

02. Financial Crisis Accelerated West to East Power Shift 07 min 50 sec

03. American Business Culture Is Healthy 06 min 44 sec

04. Threat of Rapid Decline 03 min 53 sec

05. Complexity Theory and National Strength 02 min 30 sec

06. Debt and Stimulus 03 min 22 sec

07. Innovation Only Helps by Creating Domestic Jobs 02 min 59 sec

08. Growing Education Gap 02 min 38 sec

09. A World Without a U.S. Superpower 04 min 55 sec

10. Q1: U.S. Headed Toward Capitalism or Socialism? 02 min 48 sec

11. Q2: What Happened to Budget Surplus 02 min 00 sec

12. Q3: Coping with China Graduating Thousands of Engineers 02 min 37 sec

13. Q4: How to Manage the Deficit 05 min 05 sec

14. Q5: Low Birth Rate in China 02 min 52 sec

15. Q6: Federal Reserve and Treasury Contribution to Crisis 03 min 26 sec

Saturday, January 22

Photo of the Day: Paul Volcker Puffing Away Circa 1980

From Floyd Norris' optimistic piece on the implementation of the Volcker Rule, which aims to ban proprietary trading at systemically important financial institutions (aka Too Big Too Fail) in today's NY Times.

You might be smoking like a chimney too if you had to explain to Congress how you were going to avoid causing massive unemployment (and cost pols their re-election) while slaying double digit inflation.

|

| Former Federal Reserve Chairman Volcker testifying before the U.S. House Banking Committee, 1980 |

You might be smoking like a chimney too if you had to explain to Congress how you were going to avoid causing massive unemployment (and cost pols their re-election) while slaying double digit inflation.

Greenspan's Opinion on the Gold Standard and Where's Gold Heading Now?

Some choice comments on gold from the former Federal Reserve Chairman previously made on Fox Business News:

Contrary to what the occasionally conspiratorial and always hyperbolic 'Tyler Durden(s)' of ZeroHedge would have you believe, these quotes (while perhaps deserving of a muted 'wow' from those hearing them for the first time) aren't nearly as big of a surprise as World Bank President Bob Zoellick's recent call for a return to the Gold Standard.

Throughout his career Greenspan hasn't exactly been shy about making his feelings about Au known. Further, Greenspan is a highly paid private consultant right now without any official government responsibilities or gag orders. He (and his clients) are no doubt aware that his words still carry significant weight in the marketplace, and he can say whatever he likes and even talk his own book.

Throughout his career Greenspan hasn't exactly been shy about making his feelings about Au known. Further, Greenspan is a highly paid private consultant right now without any official government responsibilities or gag orders. He (and his clients) are no doubt aware that his words still carry significant weight in the marketplace, and he can say whatever he likes and even talk his own book.

Having said that, as a close student of Greenspan's philosophy and personality I can say with a high degree of certainty that he very much cares about his place in history, particularly at this stage in his career.

In other words, the likelihood that the former Chairman is going on television and talking up gold the past few years just to earn a few bucks from hedge funds is low, in my opinion. And with outgoing Fed Governor Thomas Hoenig also recently weighing in on the yellow metal's merits one can't help notice the growing chorus for a reconsideration of the gold standard.

Continue reading the full article published on SeekingAlpha here.

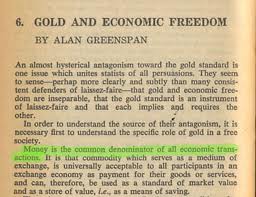

"We have at this particular stage a fiat money which is essentially money printed by a government and it's usually a central bank which is authorized to do so. Some mechanism has got to be in place that restricts the amount of money which is produced, either a gold standard or a currency board, because unless you do that all of history suggest that inflation will take hold with very deleterious effects on economic activity. There are numbers of us, myself included, who strongly believe that we did very well in the 1870 to 1914 period with an international gold standard."During the interview Greenspan also wondered aloud whether we really need a central bank.

Contrary to what the occasionally conspiratorial and always hyperbolic 'Tyler Durden(s)' of ZeroHedge would have you believe, these quotes (while perhaps deserving of a muted 'wow' from those hearing them for the first time) aren't nearly as big of a surprise as World Bank President Bob Zoellick's recent call for a return to the Gold Standard.

Having said that, as a close student of Greenspan's philosophy and personality I can say with a high degree of certainty that he very much cares about his place in history, particularly at this stage in his career.

In other words, the likelihood that the former Chairman is going on television and talking up gold the past few years just to earn a few bucks from hedge funds is low, in my opinion. And with outgoing Fed Governor Thomas Hoenig also recently weighing in on the yellow metal's merits one can't help notice the growing chorus for a reconsideration of the gold standard.

Continue reading the full article published on SeekingAlpha here.

Friday, January 21

Thursday, January 20

Video: On Why Becoming More Energy Efficient is Simply Not Good Enough

"Like salt, we need to strip oil of its strategic importance."

-Gal Luft, Executive Director of the Institute for the Analysis of Global Security and a founder of the Set America Free Coalition

The word 'independence' implies choice, and when it comes to an energy source for automobiles the vast majority effectively have zero choice.

For a long time now oil has had a monopoly as THE energy source used in vehicle transportation, and we must find a way to put an end to oil's stranglehold.

Luft's and coauthor Anne Korin's book, titled Turning Oil into Salt: Energy Independence Through Fuel Choice, argues for the importance of making oil as un-strategic a commodity as salt has become.

Many have forgotten or never learned that wars used to be fought over salt. The 'primordial condiment' as some have called it was one of the most effective ways to preserve food, making it perhaps the world's most strategic commodity.

|

| Nissan Leaf |

Their book can be found in the Good Books and Films section on the right side of this blog.

The Key Reason Electric Vehicles Matter

While most of a recent Seeking Alpha article titled 'Plug-in Vehicles and Their Dirty Little Secret' with 444 comments and counting is correct, there's a lot more to the electric vehicle story than the author's focus on emissions would lead the reader to believe.

EV Emissions and the Present and Future Grid

From an emissions perspective, running your car on electricity is about 25% cleaner than a standard car that gets about 25 mpg. But compared to a hybrid that gets more like 45-50 mpg, electric cars produce more emissions (e.g., carbon).

It's also true that more charging will likely occur at night, when the power produced is more heavily coal-weighted. However, while charging at night is worse from an emissions perspective it is much better from a grid stability and grid transmission perspective.

It's also worth noting that the mix of generation sources that provide power to the grid is changing - it is getting cleaner. Coal's share of the gird (in the U.S.) has gone from ~55% in the late 1980s to ~45% today. This trend will continue, especially as the U.S. continues to retire many of its older coal plants and replaces them with natural gas power plants, and more wind/solar.

The Environmental Protection Agency continues to tighten emissions regulations on power plants, so even newer coal plants (the few that will get built) are much cleaner and more efficient than the current ones. So using today's grid mix in assessing EVs ignores the improvement in emissions we'll be seeing in the future as the grid becomes cleaner.

How Much Do Electric Cars Really Cost?

There is one misleading remark the author makes on cost: in many cases running your car on electricity is actually cheaper than gasoline. $3.00/gal gasoline for a car that gets 30 mpg = $0.10/mile. If that car ran on electricity, it would get about 3 miles / kWh, and so for an electricity cost of $0.12/kWh (the US average), that works out to only $0.04/mile, or 60% less.

But this is only one example. Californians pay a lot for electricity, so it could be more expensive to run the car on electricity. Note: PG&E is working on rate structures that make it cheaper to charge at night, thus helping improve the economics for electric cars.

However, the cost of battery packs is expensive, so if you amortize the cost of the battery pack over the lifetime mileage of the pack, then that cost/mile obviously goes up for EVs. But is it really fair to do that? Do we similarly amortize the cost of a gasoline engine, fuel system, tank, etc? No. But without question, these battery packs are expensive, so the costs of the cars will be higher.

Why Electric Vehicles Truly Matter

So what's really behind all this fuss about rechargeable cars? If it's not about saving money, and not about reducing emissions, then what's left?

Energy security.

The biggest challenge our worldwide energy system faces is the near complete monopoly that oil has on the transportation sector. We heat our homes using a variety of energy sources. We make electricity using a variety of energy sources. But when it comes to the 3rd category of energy consumption (transportation) it is essentially all oil.

And making things worse is the fact that the U.S. imports about 2/3 of its oil, and 40% of those imports come from OPEC. This is not a very encouraging situation for whole host of reasons and warrants a separate article.

Hybrids help reduce oil consumption, which is obviously good for reducing emissions, fuel costs, and it helps reduce dependence on oil imports. But it does little to break oil's monopoly on the auto and overall transportation sector.

We need to find alternatives to oil, and the longer we wait the more painful it will become.

(Note: for more information on electric vehicles check out MIT's EV team page here and this recent report from the MIT Energy Initiative.)

EV Emissions and the Present and Future Grid

From an emissions perspective, running your car on electricity is about 25% cleaner than a standard car that gets about 25 mpg. But compared to a hybrid that gets more like 45-50 mpg, electric cars produce more emissions (e.g., carbon).

It's also true that more charging will likely occur at night, when the power produced is more heavily coal-weighted. However, while charging at night is worse from an emissions perspective it is much better from a grid stability and grid transmission perspective.

It's also worth noting that the mix of generation sources that provide power to the grid is changing - it is getting cleaner. Coal's share of the gird (in the U.S.) has gone from ~55% in the late 1980s to ~45% today. This trend will continue, especially as the U.S. continues to retire many of its older coal plants and replaces them with natural gas power plants, and more wind/solar.

The Environmental Protection Agency continues to tighten emissions regulations on power plants, so even newer coal plants (the few that will get built) are much cleaner and more efficient than the current ones. So using today's grid mix in assessing EVs ignores the improvement in emissions we'll be seeing in the future as the grid becomes cleaner.

How Much Do Electric Cars Really Cost?

There is one misleading remark the author makes on cost: in many cases running your car on electricity is actually cheaper than gasoline. $3.00/gal gasoline for a car that gets 30 mpg = $0.10/mile. If that car ran on electricity, it would get about 3 miles / kWh, and so for an electricity cost of $0.12/kWh (the US average), that works out to only $0.04/mile, or 60% less.

But this is only one example. Californians pay a lot for electricity, so it could be more expensive to run the car on electricity. Note: PG&E is working on rate structures that make it cheaper to charge at night, thus helping improve the economics for electric cars.

However, the cost of battery packs is expensive, so if you amortize the cost of the battery pack over the lifetime mileage of the pack, then that cost/mile obviously goes up for EVs. But is it really fair to do that? Do we similarly amortize the cost of a gasoline engine, fuel system, tank, etc? No. But without question, these battery packs are expensive, so the costs of the cars will be higher.

Why Electric Vehicles Truly Matter

So what's really behind all this fuss about rechargeable cars? If it's not about saving money, and not about reducing emissions, then what's left?

Energy security.

The biggest challenge our worldwide energy system faces is the near complete monopoly that oil has on the transportation sector. We heat our homes using a variety of energy sources. We make electricity using a variety of energy sources. But when it comes to the 3rd category of energy consumption (transportation) it is essentially all oil.

And making things worse is the fact that the U.S. imports about 2/3 of its oil, and 40% of those imports come from OPEC. This is not a very encouraging situation for whole host of reasons and warrants a separate article.

Hybrids help reduce oil consumption, which is obviously good for reducing emissions, fuel costs, and it helps reduce dependence on oil imports. But it does little to break oil's monopoly on the auto and overall transportation sector.

We need to find alternatives to oil, and the longer we wait the more painful it will become.

(Note: for more information on electric vehicles check out MIT's EV team page here and this recent report from the MIT Energy Initiative.)

Tuesday, January 18

Bravo Sir John Vickers, the 'Too Big to Fail'-Slaying Hero

|

| Sir John Vickers |

Sir John Vickers, head of the U.K.'s commission on banking reform, is making it clear that Too Big to Fail's days are numbered.

And the change can't come soon enough. Following Iceland's financial collapse, Britain's economy arguably became the world's most overbanked and vulnerable to an even greater systemic financial crisis than the most recent one.

The City of London is home to three of the world's five largest banks by assets (Royal Bank of Scotland, HSBC, and Barclays), and the total assets of the U.K.'s banking sector are approximately 5X the size of the nation's GDP (Iceland's banks' were 10X before its banks collapsed).

We wish Vickers luck with his efforts to put a stake through the heart of what I call 'Too Bigger to Fail' as it won't be easy sailing. Encouragingly, Sir John has proven himself to be capable of driving controversial and difficult institutional change; previously he was responsible for eliminating the notorious three hour exam on a single word at Oxford's ultra traditional All Souls College.

And we further hope that England's former compatriots across the Atlantic are taking note, for Britain can't do this alone. International cooperation and solidarity are crucial to solving this problem.

Sunday, January 16

U.S. Debt Interest Payments to Surpass Defense Expenditures Within Decade

The Congressional Budget Office is estimating that annual interest payments on federal debt will more than double over the next decade to $778 billion.

Put another way, the U.S. will soon be paying federal debt interest (much of it to Asian and Middle East creditors) equal to the U.S.'s annual defense budget.

What assumptions lay behind the CBO's estimates? From the WSJ:

Whether the U.S. will actually be able to borrow long-term at a (historically) relatively low 5-6% interest rate in a decade's time is pure speculation by the CBO.

Whether the U.S. will actually be able to borrow long-term at a (historically) relatively low 5-6% interest rate in a decade's time is pure speculation by the CBO.

I'd also like to better understand why the CBO is projecting that U.S. interest rates across the yield curve will dramatically flatten? Right now the U.S. pays an interest rate of roughly 0.15% on 3-month borrowings, while the 10-year note is yielding 3.32%, for a difference of over 3% between short-term and longer-term borrowings. That's a pretty significant difference compared between the current level and the 0.9% difference the CBO is projecting in 2020.

If the U.S. continues its current debt trajectory is it reasonable to assume that it will be able to borrow long-term at a mere couple percentage points higher than today's levels?

Professor Barry Eichengreen is predicting that emerging financial powerhouses, such as China, will be able to offer a reserve currency alternative to the U.S. Dollar by 2020. The U.S. is undoubtedly realizing lower interest rates right now due to the European sovereign debt crisis, and the lack of any real alternatives to the U.S. dollar as the world's primary reserve currency and the unparalleled liquidity of the U.S. treasuries market. What will happen when (not if) the situation changes?

Interest rates can certainly rise faster and/or higher than the CBO is projecting. A recalculation by the bond market of the U.S.'s credit worthiness can occur suddenly, as we saw last year with Greece. Professor Niall Ferguson for one is predicting that a U.S. fiscal crisis, similar to the one experienced by Greece last year, will occur within 2-4 years.

Put another way, the U.S. will soon be paying federal debt interest (much of it to Asian and Middle East creditors) equal to the U.S.'s annual defense budget.

What assumptions lay behind the CBO's estimates? From the WSJ:

As bad as that sounds, I believe the CBO could be painting an overly optimistic scenario.In 2010, it (the U.S. federal government) paid an average of about 0.1% interest on 3-month Treasury bills, and 3% on ten-year notes. Total net payments amounted to $197 billion, or 1.4% of annual economic output. That’s a bit more than what the government spent on unemployment insurance.Low interest rates, however, won’t last forever — assuming the U.S. economy doesn’t succumb to long-term, Japanese-style stagnation. The CBO estimates that interest rates on 3-month bills and 10-year notes will reach 5.0% and 5.9%, respectively, by 2020. That, together with a rapidly rising debt load, would cause annual net interest payments to more than double by 2020 — to $778 billion, or a record 3.4% of GDP.

I'd also like to better understand why the CBO is projecting that U.S. interest rates across the yield curve will dramatically flatten? Right now the U.S. pays an interest rate of roughly 0.15% on 3-month borrowings, while the 10-year note is yielding 3.32%, for a difference of over 3% between short-term and longer-term borrowings. That's a pretty significant difference compared between the current level and the 0.9% difference the CBO is projecting in 2020.

If the U.S. continues its current debt trajectory is it reasonable to assume that it will be able to borrow long-term at a mere couple percentage points higher than today's levels?

Professor Barry Eichengreen is predicting that emerging financial powerhouses, such as China, will be able to offer a reserve currency alternative to the U.S. Dollar by 2020. The U.S. is undoubtedly realizing lower interest rates right now due to the European sovereign debt crisis, and the lack of any real alternatives to the U.S. dollar as the world's primary reserve currency and the unparalleled liquidity of the U.S. treasuries market. What will happen when (not if) the situation changes?

Interest rates can certainly rise faster and/or higher than the CBO is projecting. A recalculation by the bond market of the U.S.'s credit worthiness can occur suddenly, as we saw last year with Greece. Professor Niall Ferguson for one is predicting that a U.S. fiscal crisis, similar to the one experienced by Greece last year, will occur within 2-4 years.

Saturday, January 15

{kind=link}

Quote of the Day: Jim Rogers On Why He's Long Cotton

“Paper money is made of cotton, and I’m long cotton, by the way,” Rogers said. “One reason I’m long cotton is because Dr. Bernanke is out there running the printing presses as fast as he can.”More from Rogers, including his thoughts on gold, can be found here.

Thursday, January 13

Ken Rogoff Forecasts "Currency Chaos" in 2011

Note to U.S. dollar bears: Rogoff points out that the U.S. dollar's "purchasing power is already scraping along at a fairly low level globally – indeed, near an all-time low, according to the Fed’s broad dollar exchange-rate index. Thus, normal re-equilibration to “purchasing power parity” should give the dollar slight upward momentum."

Video: Niall Ferguson -- Empires on the Edge of Chaos

Featured on FORA.tv, broken out in subject chapters in the links below. Be sure to check out the Q&A.

01. Introduction 09 min 09 sec

02. Niall Ferguson Opening Remarks 01 min 40 sec

03. Historical Cycles of Empire Decline 07 min 07 sec

04. Complexity Theory 08 min 20 sec

05. Implications for the United States 06 min 22 sec

06. Interest Payments as a Share of US Revenue 01 min 56 sec

07. Failure of Perception 02 min 43 sec

08. Debt Payment Overtaking Defense Spending 06 min 58 sec

09. Q1: Healthcare Reform 04 min 10 sec

10. Q2: China's Military Sustainability 02 min 38 sec

11. Q3: Gold Investing 01 min 24 sec

12. Q4: Political Stability of China 02 min 42 sec

13. Q5: Children Teaching You About Debt / Radical Islam 03 min 57 sec

14. Q6: Advice to Obama 02 min 40 sec

15. Q7: Limits of Keynesian Stimulus 03 min 46 sec

16. Q8: Better Leadership in the West 03 min 27 sec

17. Q9: Fear of Hyperinflation 05 min 09 sec

01. Introduction 09 min 09 sec

02. Niall Ferguson Opening Remarks 01 min 40 sec

03. Historical Cycles of Empire Decline 07 min 07 sec

04. Complexity Theory 08 min 20 sec

05. Implications for the United States 06 min 22 sec

06. Interest Payments as a Share of US Revenue 01 min 56 sec

07. Failure of Perception 02 min 43 sec

08. Debt Payment Overtaking Defense Spending 06 min 58 sec

09. Q1: Healthcare Reform 04 min 10 sec

10. Q2: China's Military Sustainability 02 min 38 sec

11. Q3: Gold Investing 01 min 24 sec

12. Q4: Political Stability of China 02 min 42 sec

13. Q5: Children Teaching You About Debt / Radical Islam 03 min 57 sec

14. Q6: Advice to Obama 02 min 40 sec

15. Q7: Limits of Keynesian Stimulus 03 min 46 sec

16. Q8: Better Leadership in the West 03 min 27 sec

17. Q9: Fear of Hyperinflation 05 min 09 sec

Wednesday, January 12

Above the Law? All Quiet in the U.S.-U.N. Spy Scandal

|

| U.N. Secretary General Ban Ki-Moon and Hillary Clinton |

To recap, State Department Secretaries Hillary Clinton (Democrat) and Condoleeza Rice (Republican) both instructed U.S. foreign service personnel and diplomats to obtain a wide variety of information about U.N. officials, including the following:

- DNA

- Fingerprints

- Iris scans

- Computer passwords

- Credit card numbers

- Personal encryption keys

What Precisely Constitutes 'Spying'?

While I'm not a legal expert on what constitutes 'spying' (which is banned from being performed against the U.N. under international treaty and law), the above laundry list (which once collected by State's 'diplomats' was handed over to the CIA's HUMINT department) sounds an awfully lot like 'spying' to me.

|

| The Formers: U.S. and U.N. Secretaries Rice & Annan |

Clinton and Rice signed off on orders instructing diplomats to obtain this type on information "on key UN officials, to include undersecretaries, heads of specialised agencies and their chief advisers, top SYG [secretary general] aides, heads of peace operations and political field missions, including force commanders".

Another angle here is that the U.N. human data collection project, rather than having been carried out by CIA clandestine ops, appears to have been performed by State's foreign service officers and other diplomatic personnel. One of the purported goals of U.S. diplomats is to build relations and trust among foreign nations. What impact has the disclosure that these individuals are engaged in the gathering of the DNA samples of foreign diplomats had on this important function?

Where's the Followup?

I've been waiting to hear an announcement of an investigation, or perhaps at least rumors of an internal State department review. But so far there has not been one peep of anything like this.

Is it possible that the reason behind why no further investigation is that international treaty only outlaws spying agains the U.N. and its officials on U.N. premises? In other words, all U.S. State department spying on U.N. officials took place offsite?

Or, in a perhaps somewhat more conspiratorial vein, is the lack of follow-up due to the fact that the source of the spying information is WikiLeaks? One way to limit the credence of all WikiLeaks disclosures and move the leaks out of the headlines is to not pursue any of the potentially illegal activity disclosed by WikiLeaks. This may also serve as a disincentive to future prospective leakers.

One of the most interesting elements of the the recent WikiLeaks disclosures was the near uniform international condemnation of WikiLeaks and, as far as I could tell, almost complete lack of criticism directed at the U.S. by foreign sovereigns. Perhaps this is simply a case of the pot not wanting to call the kettle black; I have little doubt that Putin's Russia, for example, engages in similar espionage.

One of the most interesting elements of the the recent WikiLeaks disclosures was the near uniform international condemnation of WikiLeaks and, as far as I could tell, almost complete lack of criticism directed at the U.S. by foreign sovereigns. Perhaps this is simply a case of the pot not wanting to call the kettle black; I have little doubt that Putin's Russia, for example, engages in similar espionage.

Walking the Rule of Law Talk

There are many unanswered questions, but the bottom line for me is this: if the U.S. wants to lay claim to the moral high ground or simply preach the importance of the rule of law to countries such as Russia, China, Iran, etc., then the U.S. needs to 'walk the talk'.

Keeping mum about whether illegal spying on U.N. officials occurred only hurts the U.S.'s international standing and credibility. Instead there should be some type of investigation so that U.S. citizens, and the world at large, can be confident that U.S. leaders and diplomatic staff respect and uphold agreed upon laws.

Wall St. & Obama's $1 Billion Presidential Re-Election Fundraising Goal

And now with Obama's recent appointments of officials drawn from 'Too Big to Fail' institutions like Bill Daley of JP Morgan Chase and Gene Sperling of Goldman Sachs to key posts in his administration, we can see where Obama expects to raise that $1 billion.

Wall Street is home to perhaps the biggest pile of campaign contributions. As Inside Job Director Charles Ferguson explains, while Obama's decision to give in to Wall Street is depressing it's entirely rationale in terms of his re-election fundraising goals.

In fact it's a pretty safe bet that both Democrats and Republicans will be aggressively courting Wall Street and the now 'Too Bigger to Fail' banks for massive 2012 presidential campaign contributions.

And I'm sure there will be no strings attached to any such contributions, right Lloyd and Jamie?

Thursday, January 6

Timing the Inevitable Decline of the U.S. Dollar

One of the most heavily debated macro topics is the future of the world's reserve currency, the seemingly almighty U.S. Dollar.

Neither the fact that scores of prognosticators have been predicting its demise for decades, nor that when the financial going gets tough (as it did during the 2008-2009 financial crisis) everyone wants it, has dissuaded today's dollar bears from taking a dim view of the greenback's future.

America's Exorbitant Privilege

Neither the fact that scores of prognosticators have been predicting its demise for decades, nor that when the financial going gets tough (as it did during the 2008-2009 financial crisis) everyone wants it, has dissuaded today's dollar bears from taking a dim view of the greenback's future.

America's Exorbitant Privilege

|

| Barry Eichengreen |

Professor Eichengreen opens with the point that while we now live in a multi-polar economic world the financial system and monetary order still revolve around a single currency (the U.S. Dollar).

Some might be surprised to learn that approximately 75% of all $100 bills circulate outside the United States. The reserve currency holdings of the world's central banks are largely in U.S. Dollars or U.S. Dollar denominated assets (e.g., U.S. Treasuries).

What precisely is the 'Exorbitant Privilege' conferred on the United States by the special role its currency plays in the global financial system?

Professor Eichengreen calculates that the U.S. dollar’s status as the world's reserve currency is worth 3% in U.S. national income per year. In other words, having the world’s dominant reserve currency allows the U.S. to run an annual $500 billion current account deficit.

Some may remember Vice President Cheney's quip that "deficits don't matter", or Nixon Treasury Secretary Connally's response to foreign governments, critical of the U.S.’s profligate Vietnam and Great Society spending, on how the U.S. Dollar was "our currency, your problem". It is this 'Exorbitant Privilege', a term coined by French leaders in the 1960s who railed against the fact that American paper currency could be exchanged for "real stuff", which Professor Eichengreen views as unsustainable.

Are Reserve Currencies Analogous to Computer Operating Systems?

Economists explain the U.S. Dollar's rise and dominance through a principle called 'network externalities' (or 'network effect'). Similar to how significant interoperability advantages in computing can be achieved through the adoption of a single operating system (e.g., Microsoft Windows), the widespread use of a single currency (the U.S. Dollar, and previously British pound sterling) can lead to mutually beneficial economic efficiencies.

However, in a world where 'Currency Converter' is one of the Top 10 most downloaded smartphone apps, determining exchange rates and making currency conversions can now be performed quickly and simply by a vast number of people. Just as the computing world is moving towards multiple operating systems (i.e., Windows, Mac, Linux, Google, iOS, etc.), Eichengreen believes the world will transition to three principal reserve currencies: the U.S. Dollar, the Euro, and the Chinese Renminbi (Yuan).

The Euro and the Renminbi: Assessing the U.S. Dollar Bridesmaids

On the currency topic du jour, Eichengreen believes that "euro gloom and doom is overdone". Just as a default by Los Angeles County won't spell the end of the U.S. Dollar, a default by Greece and/or Ireland won't bring about an end to the euro.

Germany is the one country, in Eichengreen's view, which could afford to abandon the euro without suffering catastrophic economic consequences. However, Eichengreen sees this as unlikely. Germany's next generation of leaders, while not having been around for the birth of the EU, are nevertheless heavily wedded to the European Project. Further, Germany benefits from a weaker euro via more competitive exports. If Germany were to leave the euro then the reintroduced Deutsche Mark would shoot up in value and risk choking off the German export led economic renaissance currently underway.

When it comes to the Chinese renminbi becoming a reserve currency, Eichengreen acknowledges that China needs to make significant changes. For starters, the renminbi will need to become freely convertible. China will also need to develop deep, liquid capital markets and make fundamental changes to its overall development model.

However, these and other changes may come quicker than many expect. A short time ago there were basically zero Chinese companies settling international transactions in renminbi; now 70,000 do so. Two U.S. multinational companies, McDonald's and Caterpillar, have issued renminbi-based bonds. Currently most of these changes are occurring in "China's financial petri dish" (Hong Kong), but China has set a target of making Shanghai a preeminent world financial center by 2020.

Timing the Decline of the U.S. Dollar?

Eichengreen assigns a very low probability to a sudden collapse of the U.S. Dollar. But could it happen? In short, the answer is yes.

A spat over Taiwan or rising tensions in the Asia Pacific over China building its first world class navy in 600 years could cause China to suddenly stop funding U.S. deficits. A more confident and assertive China is likely to continue to flex its newfound muscles, a subject I previously covered in more detail here.

However, what Harvard’s Larry Summers termed "The Financial Balance of Terror" is likely to prevent a catastrophic scenario from unfolding. Similar to how President Eisenhower threatened to dump the U.S.'s vast British bond holdings during the 1956 Suez crisis if British forces didn't leave the peninsula immediately (which they did), Eichengreen believes that China and U.S. officials will attempt to work out their differences through diplomatic back channels as opposed to openly fighting it out in financial markets.

A more likely scenario would be a sudden loss in investor confidence, like the one experienced by Greece last spring, in the U.S.'s ability to get a handle on government spending. Eichengreen notes how the ratio of U.S. federal debt (a relatively high 75% of GDP) vis-à-vis tax revenues (a relatively low 19% of GDP) is rapidly approaching the danger zone.

From an investment perspective, investors should continue to expect currency volatility under the current U.S. dollar dominated international monetary system. Further, the U.S. Dollar will continue to be the world's safe haven currency in times of crisis for the foreseeable future. However, according to Eichengreen a change in the international monetary order is all but inevitable within a decade.

Subscribe to:

Posts (Atom)